Work, Play and the Fortunate Kind

This week marks the unofficial end to summer, at least from the perspective of the investment business. That’s because next week, trading desks will start to get back to full staff after the Labor Day respite on Monday.

It’s always interesting to me to see the trading volume decline in a week prior to a big holiday weekend, as most people — including the biggest money managers — have virtually “checked out” to enjoy the next 90-plus hours left before Tuesday’s opening bell.

As for me, I don’t check out, ever, because I think life should be all about the integration of work and play. To me, they’re the same thing, which means I’m always working and always playing — and that makes me a member of the fortunate kind, the kind whose work is his play and vice versa.

So, what should we expect when the rest of the world gets back to the business of trading next week?

Well, given that domestic stocks now are sitting just below all-time highs, we have to ask ourselves: what catalysts can either A) Send stocks markedly higher into the end of the year or B) Cause a significant reversal in this summer rally?

I’ll be looking at each of the following catalysts closely over the next several weeks, as the answers will start to come in fast and furious. However, today I want to simply sketch out a few highlights from the catalysts I think most likely to affect the markets for the next several months.

These catalysts are ranked in order of importance (i.e. ranked by their respective ability to cause a rally or a pullback). And, big thanks to my friend and market genius, Sevens Report editor Tom Essaye, for his advice and counsel in assessing the following catalysts.

1) U.S.-China Trade Deal. This has been the biggest catalyst on markets all year, so it’s no surprise it will continue to be the biggest catalyst going forward. If we see an actual deal between the United States and China on trade, I suspect the bulls will suck that up like an energy drink and keep running all the way to 2019. If, however, there’s no trade deal struck and more tariffs go into place, then we’ll likely see the bear break out and wrestle control away from what can certainly be considered an aging, if not downright tired, bull. Next Key Event/Date: Sept. 5, which marks the end of the “comment period” for the proposed 25% tariff on $200 billion in Chinese exports.

2) December Fed Rate Hike. There are rumblings out there that the Federal Reserve may press the pause button on a December rate hike (a September rate hike is a virtual certainty). Last week, both the Federal Open Market Committee (FOMC) minutes and a speech by Fed Chair Powell had slightly “dovish” tones, and there is a growing expectation (but not consensus) that the Fed will pause for a bit after the September hike. If the Fed does press the pause button in December, it will be viewed as a positive for the bulls. Key Event/Date: Sept. 26, the next Fed meeting, which should give us clues about a December hike.

3) U.S. Dollar. The rising value of the U.S. dollar vs. rival foreign currencies has become a headwind for stocks of late, and that’s because if the dollar keeps rising it will pressure Q3 corporate earnings as well as global growth. If we see the dollar start to come back down, that will be a positive for equities. If, however, the dollar keeps pushing higher, that will strengthen the headwinds… and that could finally trip up the bulls.

4) Q3 Earnings Season. Above all else, the 2018 rally has been primarily earnings-driven. That means that for stocks to continue pushing higher, earnings must continue to grow. If that doesn’t happen, and if earnings start to get pressured for any reason (stronger dollar, lack of economic momentum, tariffs, etc.) then this market will develop a valuation problem, and that could take stocks down quickly. Next Key Event/Date: Oct. 8, the first week of the Q3 reporting season.

5) Midterm Elections. If I must put on my political hat (a hat I prefer to leave in the closet), I am forced to conclude that the midterm elections will likely result in a split Congress (Democrats in control of the House, Republicans in control of the Senate and the White House) and a stalemated government. That’s a good thing for markets, historically speaking; however, today’s political environment is nothing if not a historical anomaly. If the political headlines surrounding President Trump and the Mueller investigation begin to look dire for the administration, then we could see political drama that even the most intrepid bulls would find difficult to escape. Next Key Event/Date: Election Day, Nov. 6.

Again, I’ll have more on each of these catalysts in the hotlines and in our monthly newsletter. For now, know that I will be watching each of these potential catalysts closely to help us determine the next direction for stocks now that the summer trading season is over.

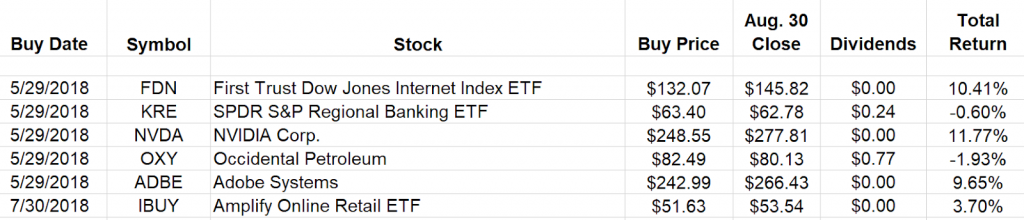

As the summer comes to a close, we are sitting on some great gains in the TTP portfolio. We now have double-digit-percentage gains in the First Trust Dow Jones Internet Index ETF (FDN) and NVIDIA Corp. (NVDA), as well as a near-double-digit-percentage gain in Adobe Systems (ADBE).

Finally, I hope you have a tremendous weekend. I know I plan to do what I do best this Labor Day — and that is to combine work and play such that there is zero distinction between the two.

Search